Board Member Seeks Digital Revolution

| HEY OGI, I would really like your opinion on something… [Name removed]’s (our current manager) excuse for not doing some work digitally, such as [buyer] applications, is that sensitive financial information such as tax returns, can be easily leaked over email. What is the way around this? Aside from putting everything on a CD four times and then distributing to the Board by hand … can’t there be a more secure way of forwarding such information to the Board, like posting it temporarily on a secure page or secure inbox for their review?Can you please put in your two cents, I’d really really appreciate it. I understand that Recognition Agreements (and I believe, the Commitment Letter) have to be signed and sealed originals but that is easily done after a review of the whole package. Our management company charges us $50 for a credit check and $250 for an application fee (besides the $450 we pay to the Coop) for doing very very little. BEST,  |

DEAR UNDER THE LUDDITE’S THUMB, Our two cents? You are being taken advantage of. Sensitive financial information can indeed be leaked over email. However, that doesn’t justify making your role as a board member more difficult. Regardless of how the confidential documents are distributed to the board, it is up to each board member to make sure they handle the information responsibly. Your contact is using that explanation to hide backward or out of date technology practices. One way around this could be a password protected website or webpage. Decent managers can can give different levels of access to board members, residents, etc. Nothing is foolproof, but some systems make property owners’ lives easier than others. Paper is the worst for many reasons (cost, speed, trackability, environmental impact etc.). Even so, as you mention, some documents still require original signatures. On those, there’s no way around paper. A $50 credit check and $250 processing fee are industry standard. Neither is a bargain, but neither should change a board member’s vote. They are both usually passed through to renters or new purchasers. Two forces that drive private sector processes should be ease of use and customer service. When you have trouble finding these with your vendors, start looking for alternative solutions. WARM REGARDS, THE OGI TEAM |

Going Green, After Construction It’s All About Process

The post construction processes that contribute meaningfully to a building’s carbon footprint include the lighting, thermal envelope (whether or not a building leaks heat), bill collection and check writing. Yes, bill collection and check writing. Not surprisingly, these items correspond to line items from a property’s expense list.

Through online payment transfers, savvy property owners can both increase their ROI (shorter cash conversion cycle), decrease lost payments (the USPS is no internet), and decrease a building’s carbon footprint (no killed trees, far lower carbon emissions). Next generation property management is embracing online payment transfers and reporting for those reasons. This isn’t just green business, it’s good business.

In rental buildings, tenants want to live in a healthier, greener environment. Although this remains difficult to quantify, it makes them feel good about their choice of buildings. There is mounting evidence that tenants are willing to pay a green premium over market rents.

The best way to justify, implement, and embrace change is to regard it as improvement. When property owners consider the multiple advantages of green processes, they need to include the good they do for the environment and their wallets. Better, greener processes should benefit current owners here. Not only will owners lower their current operating costs, but also improve their exit prices down the road. One clear aspect of real estate that future purchasers will investigate is how much a building costs to run. A less clear aspect of real estate value that purchasers look at is how green a building is and what steps management has taken to reduce the carbon footprint. Although difficult to measure, the panache associated with being green translates indirectly to the bottom line. People pay up for and buy more quickly into green property.

This seems a fitting topic as we wind down Earth Month- going green for all the right reasons. The owners who emerge first and best from this market will be the ones who have listened to the market, offer what people want and manage their properties best. As commercial and residential vacancies climb and late payments age, the importance of controlling what you can for your property remains paramount. When your actions can help the planet and line your wallet, so much the better.

Looking for Guidance in This Real Estate Market

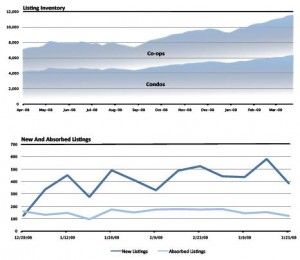

As the value of New York Real Estate evaporates, it has been difficult to accurately measure and report the speed of the decline and where real estate values have held up best. Several sources publish guides from different perspectives using different data.

One of the best, Streeteasy.com’s quarterly guide, came out last week. Aside from painting a bleak picture of the market (sales volume continues to fall) and highlighting neighborhoods where people most overpaid in recent years (Soho), the guide offers a similar purview to other reports such as Corcoran or Elliman with more emphasis on the various stages of residential real estate transactions. Reflecting its web roots, the report uses data cutting across brokerages and delivers detailed stats and graphs.

Market wide stats such as inventory,

Guide for Renters

Tips for Renters

Midtown West: the destination for non-doorman units. Midtown West has long been a neighborhood known for a central location and good value, but that value has gotten even better. With non-doorman units falling over 3% this month, apartments in this area have become an even better bargain. Non-doorman studios are now the lowest priced units, with the exception of Harlem, at $1,670.

Clear choice: LES. If you’re looking for a one-bedroom apartment with service, forget the rest of Manhattan, renters should be combing the LES for deals. One-bedroom units are currently averaging $2,547 – over $450 cheaper than any other central Manhattan location.

Safety, security and service. Battery Park City prices have continued to fall from their heights of last spring and summer. Units in this area are down an average of 14% from their peaks, making them an excellent value for those looking for service and a quieter location.

What does it all mean? There aren’t many surprises here. Values are falling and will continue to fall. Corcoran’s report had a nice conclusion about this, drawing on Robert Shiller, co-creator of the Case-Shiller Home Price Index. “As early as 2005 Shiller predicted severe declines in home prices across the United States. Busts, Shiller argues, follow booms. But just as surely, he says, recoveries follow busts.” In the meantime, property owners need to look for economical ways to differentiate their buildings. There are answers and these answers are not in these published guides.

Condo Dues Defaults Will Punish Unfairly and Scar the Innocents

Financially sound condominium owners will be among the next groups victimized by the credit crisis. While shaky owners default and buildings’ fees rise, that financial burden will fall squarely on the shoulders of better-positioned owners. The problems that led to this situation are sending disastrous ripples to areas that few had predicted. Laws that protect Co-op owners require any repossessing bank to pay maintenance. In a co-op, equity reverts to the building. A condo lacks this protection. With a condominium, the bank has or –in these times- lacks the equity.

Liens, Times and Years. Oh My!

A building can place liens, or threaten to, before the customary three months. Processing a lien can take many years. We got into this financial mess by assuming that existing circumstances will be similar to historical trends. It’s wake up time for the people with the ability to act.

Proactive measures for Condo boards. How early is too early?

Property managers can look for early signs of delinquency. Impose STIFF, eye-popping fines on late dues payers. The owners willing to accept eye-popping penalties are the ones with no choice. This serves as an early warning sign. Proactively filing liens on these condominium owners may get them to repay quickly. It could also be the call to face the music and downsize or seek financial help.

Another less discussed and highly likely scenario is that the courts will become backed up with foreclosure actions. The proactive boards that act swiftly in 2009 are the ones more likely to benefit.

Likely suspects

Owners who financed with no money down and or those who used the 421 tax abatement will face huge increased charges. If 40% of your building’s units have changed ownership in the past 3 years, your neighbors may have taken advantage of easy money and over leveraged themselves.

Blame the Victim?

Looking to victims for help will not provide the best solutions. Although rising delinquencies can lead to finger pointing in the micro-culture of a building (making for tense elevator rides, long board meetings and possibly officer turnover), the people most likely to solve the problem are not the ones who caused it. That unfortunate financial burden will rest with the remaining owners. The time for buildings to offer less and charge more is rapidly approaching.

A difficult pill to swallow

A difficult pill to swallow

To help, buildings can repurpose assets for income generation – storage areas for commercial or medical rentals, rooftops for solar panels or cell towers. Lighting can be switched to high efficiency fluorescent, saving thousands of dollars per year. All systems- ex. furnace gas or oil- can be evaluated for efficiency. These are potential band-aids. In the meantime, many will be injured.

Boards can implement or increase flip charges (transfer fees), and sublet charges and while decreasing required sublet lengths of stay. They can actually welcome sublets in order to increase revenue and to help the struggling owner. Health club hours can be shortened, and other amenities trimmed. These measures have traditionally been associated with Co-ops. We expect to see more condo boards instituting co-ops style policies where possible.

There is no easy fix and the problem will get worse before it gets better. The best way out of this problem is to adopt proactive measures and remain ahead of the curve.

The board of managers…shall have a lien on each unit for the unpaid common charges thereof, with interest thereon, prior to all other liens except only

(i) liens for taxes on the unit in favor of any assessing unit, school district, special district, county or other taxing unit,

(ii) all sums unpaid on a first mortgage of record,

Rent De-Regulation Costs Increase- The NY Bill Is a Monster Sans Teeth

It’s no secret that evicting non-primary tenants can be arduous, time consuming, expensive and fruitless. Now the government is trying to dissuade landlords from even trying. A bill is now pending before the NY state legislature, (A00473 see below) which would award court costs and punitive damages to tenants who successfully defend against their eviction (and against the ending of rent regulation for that unit) based on non-primary residence. A form of this bill passed the assembly on 06/24/2008.

It’s no secret that evicting non-primary tenants can be arduous, time consuming, expensive and fruitless. Now the government is trying to dissuade landlords from even trying. A bill is now pending before the NY state legislature, (A00473 see below) which would award court costs and punitive damages to tenants who successfully defend against their eviction (and against the ending of rent regulation for that unit) based on non-primary residence. A form of this bill passed the assembly on 06/24/2008.

Although this bill might appear to have teeth, really it’s all gums. Do the math from a landlord’s perspective with me:

- A lease demands $500 rent each month for an apartment that would rent for $1200 to $3600 on the open market. Three times the rent would be a $1500 penalty

- The tenant uses free legal aid or a mom and pop law firm for a maximum of 10 hours at $250/hour. This totals $2500

- Penalty losses would equal roughly $4000. The value of the building on a conservative 5x rent roll would increase by a minimum $42,000 (5*$700*12 months), alternatively, the increased rent roll of $8,400 easily justifies the risk.

- The landlord’s legal expenses also need to be considered.

For the long-term, well capitalized landlord, the decision to deregulate remains a no brainer.

There are many ways to prove a resident is not a primary tenant. Video surveillance is one. It’s not enough to show that the primary doesn’t come home for months on end. A landlord needs to show that someone else does live in the apartment in question and that the primary tenant live elsewhere. These aren’t easy to do. Secure Watch can help. They are experts at assisting landlords in proving who lives where.

Another method is to rekey the building. That’s simply changing the front locks to use a multi-lock or other hard to duplicate key system. Only primary tenants and immediate family get keys. Primary tenants who show up to housing court without keys to their ‘home’ can look pretty foolish in front of a judge.

There are more ways than these to prove non-residence and more ways than non-residence to get an unwanted tenant out. A good property management firm is an important part of any successful suit and is aware of what happens in its buildings.

New Property Management: The Devil You Wish You Knew

Many property owners shy away from changing building managers. It’s difficult. There are long established relationships, too many ongoing projects, or our favorite ” knowledge of the property”. Baloney. Bogus. Hogwash. Bollocks.

There are few reasons to stay with a property manager and many reasons to leave. When a property management firm communicates clearly and lives up to its obligations, they should be trusted and retained. But when property owners have to perform management responsibilities, it’s time to do some head scratching and ask “So why are we paying these guys?”.

Realizing it’s time to switch managers does not ensure a smooth transition; however if you have an organized step by step plan you can have a seamless hand off.

Luckily, the Real Estate Board of New York (REBNY) has laid these out or at least established some guidelines.(See Below)

Even with the guidelines in place, communication and expectation management are imperative for a successful transition.

Although prospective clients frequently ask for our opinions about specific situations before beginning a client/vendor relationship, it is important to be aware of all pre-existing conditions at a property before we begin to manage it. Learning about non-paying tenants, decade old feuds, or rowdy neighbors can be accomplished before either party sets itself up for disappointment.

Although changing management companies can seem daunting, with the right preparation, process and right company it doesn’t have to be.

|

1) MORTGAGE INFORMATION a) Payment Book/Monthly Payments b) Name and Address of Lender c) Closing binder 2) INSURANCE a) Original Policies/Schedule b) Insurance Broker c) Pending Claims 3) LEGAL a) Corporate/Certiorari Counsel b) Pending Legal Matters c) Corporate Stock Book/Seal d) Certificate of Incorporation e) Asbestos/Engineering Survey f) Survey/Deed/Title Policy g) Board Minutes h) By-Laws/House Rules i) Offering Plans/Amendments j) Conversion Closing Binder (if applicable) 4) ACCOUNTING a) Name/Address of Firm b) Federal/State/Sales Tax Returns c) Audited Annual Reports/Budget d) 1098 Information e) RPIE/RPT Filings f) Block/Lot/Assessed Valuation g) Real Estate Tax/Water Bill h) NYC Real Property Tax i) Abatement Filings 5) PAYROLL a) Employees Earning Records b) Union Wage Contract c) Forms 940 and 941 d) Unemployment Insurance Returns e) Social Security Tax Returns f) Copies of W-4 Forms g) * Federal ID number 6) TRANSFER DEPARTMENT a) Pending Transactions b) Blank Proprietary Leases c) Resale/Sublet Requirements |

7) GENERAL a) Inventory of Building Supplies b) Certificate of Occupancy c) Building Plans d) Alteration Agreement e) Commercial/Store/Garage Leases f) Water Meter Numbers g) Name of Architect & Engineers h) Vendor/Maintenance Contracts i) Board Policies/Late Fees/Sublets j) Construction Contracts/Warranties k) Floor Plans l) Lead Based Paint Records (pre 1978 buildings) m) J 51 Documents 8 ) SHAREHOLDERS/UNIT OWNERS a) *Rent Roll (Maintenance/Common Charges) b) Collections/Arrears Report c) Payment Histories/Delinquent Residents d) *Alternate Address Listing e) Share Allocation f) Garage Sales Tax Exemptions g) Current Directors/Managers h) Shareholder/Unit Owner Files i) Guarantee Agreements, if any j) Escrow Agreements, if any k) Sublease Information l) List of Mortgagees/Lenders for each unit m) List of Mortgagees/Lenders for each unit n) Shareholder/Unit owner social security number 9) OPERATIONS a) Bank Statements/Reconciliations/All Accounts b) Paid/Unpaid Invoices c) Service Contracts d) Monthly Operating Statements e) Cash Balances Available for Transfer f) Open Purchase Orders g) Pending Service Requests h) Management Reports i) Pending Violations j) Complete Set of Keys 10) LICENSES/PERMITS a) Certificate of Operations/Oil Burner b) Annual Boiler Inspection c) Fuel Storage Permit d) Super’s Certificates of Fitness e) *MDR Card f) Local Law 10/16 Reports g) Elevator Inspections/Tests h) Miscellaneous Permits |

Foreign Investors, Local Property Managers

Property management for foreign investors requires better technology and more trust than managing for local owners. When problems arise, as they surely will, remote owners need to know that managers will handle the situation completely with no supervision and little input.

We know from experience that these owners are looking for the income without the headaches. They are paying for it, so why shouldn’t they get it? Local owners frequently retain a semi-active role with the properties- approving tenants, vetting vendors, etc. Not so with remote owners. The distance between their home and investment can increase their feelings of unease. This also necessitates greater levels of trust and reliance. Property managers can either add to unease or dispel it.

The checklist when vetting a property manager for a foreign owner of local property revolves around technology and trust/accessibility.

Trust/Accessibility:

- Assurance that bids for projects, insurance, etc. Will be competitive

- Notification of Community changes (zoning, crime, etc.)

- Reliability that rents will be competitive

- Vacancies will be kept to a minimum

- Properties will be maintained according to owner’s standards.

Technology

- Online visibility of their accounts

- Access to security camera images

- Electronic fund transfer capability

- 24 hour access via an emergency phone line.

This list isn’t exhaustive. It’s a jumping off point. You may notice these requirements differ from the needs of local owners mainly in terms of trust and oversight due to the physical distance and infrequent access logistics.

Many owners look at New York property as a long term value investing play. They need to be kept abreast of changes at the local community board level and zoning board levels. If a property is rezoned, creating more FAR, owners need to know immediately. The same goes for bars, schools, and developments opening nearby.

Regarding technology, all worthwhile property management software these days allows online access for both tenants and owners. Additionally, it’s relatively inexpensive to purchase and install security cameras and hardware to monitor property remotely. The increased sense of awareness these investments offer can be worth far more than their cost to any investor.

Modern Property Management- Managing to Metrics

Property Managers need to advocate and implement financial visibility and operating efficiency. Unlike management in many other fields, property managers have largely neglected management evolution for too long. Despite Ford developing the assembly line roughly 100 years ago, building superintendents still lack processes to replicate strong consistent results on a weekly basis. Although Automated Clearing House (ACH) has been around for years and years, most property management companies still rely on postal carriers to deliver rent/maintenance/common charges. These seem like the tips of the iceberg.

Techniques have been developed to increase efficiency and visibility in business and organizations. We aren’t suggesting superintendents become automatons or that everyone be required to link their bank accounts to their property management (though sometimes these would be improvements). Instead, we advocate increased visibility and efficiency.

Wherever possible, staff responsibilities and routines should be spelled out. This is down to the details of how staircases are cleaned top to bottom, at what times, and how long it should take. Managers should inspect the results each week and keep recorded, trackable results. This performance tracking is great for employee review and customer satisfaction.

The cash conversion cycle is another passion of ours. If, rather than traditional postal delivery (assume a minimum of two days), managers use ACH, it not only improves the cash conversion cycle, it also increases automation, making payments easier to track. Increased automation is good.

When you consider what’s important in selecting your vendors (property managers, mechanics, lawyers, dry cleaners, whatever), look for visibility and efficiency. Together these produce reliability- a characteristic we’re all looking for in our partners.

According to Inc., Cash conversion cycles for small businesses are predicated on four central factors: 1) the number of days it takes customers to pay what they owe; 2) the number of days it takes the business to make its product (or complete its service); 3) the number of days the product (or service) sits in inventory before it is sold; 4) the length of time that the small business has to pay its vendors. Inc. provided the following formulas to determine these factors:

Once a small business owner has these figures in hand, he/she can figure out the company’s cash conversion cycle by adding the receivable days to the production and inventory days, then subtracting the payables days. “That will tell you the number of days your cash is tied up and is the first step in calculating how much money you’ll want in your revolving line of credit,” Inc. concludes.

Single Unit Management

When people own property, regardless of size, they need a trusted caretaker. Frequently, they play this role themselves. If an owner isn’t up for the task, they need to hire someone else. This is even more true if the owner plans to be away frequently or for extended periods of time.

Single unit owners, usually of large apartments, have recently been inquiring whether we look after empty apartments and buildings. There seems to be a shortage of such services in NYC, despite being a commonplace service in more rural areas and for single family homes.

Here’s what to look for in a single unit manager:

- Someone who is not a house sitter. House sitters are free riders. They use your real estate and charge you for it. If you wanted someone sleeping in your bed without you, they’d better be paying you. Not vice-versa.

- A company rather than an individual. This addresses issue of liability and professionalism. Companies carry insurance, have resources such as plumbers at their disposal, and reputations to protect.

- Experience. Check references. This is not difficult yet people frequently overlook its importance. There’s no excuse for mishandling your real estate investments.

- Availability. The manager should have a 24 hour emergency line.

- Preparedness. If the manager doesn’t ask for neighbors’, super’s, and vendors’ contact info upfront then they’ll be looking for the information during an emergency. These include the oil company, building manager (if there is one), property insurance company, etc.

If you have questions, we have answers.

Strategic Advice- Do I Need More Than a Sober Super?

People ask us how property managers differ. One important difference is a focus on strategic advice vs. a focus on operations. Better property managers treat buildings as businesses- increasing shareholder value and improving cash flow. Others view their responsibilities as making sure supers are sober and avoiding violations for a building.

In 2007, we focused our efforts on increasing our clients’ property value. This year, and probably through 2009, preserving value is and will be on the tops of everyone’s list. Our clients’ focus has shifted to reflect the change from seller’s to buyer’s market. It’s no coincidence that the buildings which invested or upgraded in recent times of surplus are best positioned to see their value preserved.

Currently, when owners consider investment and return on investment, they are far more concerned with the initial investment than the return now relative to last year. Where last year building boards and owners focused on what will benefit their properties the most, they are now concerned with what will cost the least. Although clients are still looking for the largest value impact for their dollars spent, they are more conscious than ever about how many dollars they are spending.

Some projects which may have been intended to increase value or functionality last year are still being implemented but on a smaller scale or with an eye towards reduced expenses.

Two examples that I plan to discuss more fully in later posts are rooftops and Children Areas (play centers, Kid corners, children areas, RecRooms, etc.)

Rooftops

Board members and owners used to ask whether we could help them utilize their rooftops. We still get some requests for this but far more frequently clients ask us about incorporating solar technology into their roofs or building coverings. We are also asked how best to utilize undeveloped FAR.

Children Areas

One low cost way to utilize a low traffic common area is a Children’s Area (Kids’ room, Play Center, Kid corners, children areas, RecRooms, etc.). These rooms transform underutilized or unutilized areas into cheerful showplaces for young children and perspective buyers. This transformation can be accomplished in areas formerly used for a variety of purposes though personal storage, equipment storage, and workshops are likely candidates. The important factors for many owners though are the low required investment (mostly paint and time) and the perceived quality of life improvement associated with the new area. Although newspapers and websites do not yet include Children Areas in their lists of amenities, in the future they may. These areas can make the difference for buyers with children.

Having reliable and impactful solutions to these questions is what sets property managers apart. Furnishing strategic plans and providing these answers are the abilities that can make property managers trusted partners.