Board Member Seeks Digital Revolution

| HEY OGI, I would really like your opinion on something… [Name removed]’s (our current manager) excuse for not doing some work digitally, such as [buyer] applications, is that sensitive financial information such as tax returns, can be easily leaked over email. What is the way around this? Aside from putting everything on a CD four times and then distributing to the Board by hand … can’t there be a more secure way of forwarding such information to the Board, like posting it temporarily on a secure page or secure inbox for their review?Can you please put in your two cents, I’d really really appreciate it. I understand that Recognition Agreements (and I believe, the Commitment Letter) have to be signed and sealed originals but that is easily done after a review of the whole package. Our management company charges us $50 for a credit check and $250 for an application fee (besides the $450 we pay to the Coop) for doing very very little. BEST,  |

DEAR UNDER THE LUDDITE’S THUMB, Our two cents? You are being taken advantage of. Sensitive financial information can indeed be leaked over email. However, that doesn’t justify making your role as a board member more difficult. Regardless of how the confidential documents are distributed to the board, it is up to each board member to make sure they handle the information responsibly. Your contact is using that explanation to hide backward or out of date technology practices. One way around this could be a password protected website or webpage. Decent managers can can give different levels of access to board members, residents, etc. Nothing is foolproof, but some systems make property owners’ lives easier than others. Paper is the worst for many reasons (cost, speed, trackability, environmental impact etc.). Even so, as you mention, some documents still require original signatures. On those, there’s no way around paper. A $50 credit check and $250 processing fee are industry standard. Neither is a bargain, but neither should change a board member’s vote. They are both usually passed through to renters or new purchasers. Two forces that drive private sector processes should be ease of use and customer service. When you have trouble finding these with your vendors, start looking for alternative solutions. WARM REGARDS, THE OGI TEAM |

Going Green, After Construction It’s All About Process

The post construction processes that contribute meaningfully to a building’s carbon footprint include the lighting, thermal envelope (whether or not a building leaks heat), bill collection and check writing. Yes, bill collection and check writing. Not surprisingly, these items correspond to line items from a property’s expense list.

Through online payment transfers, savvy property owners can both increase their ROI (shorter cash conversion cycle), decrease lost payments (the USPS is no internet), and decrease a building’s carbon footprint (no killed trees, far lower carbon emissions). Next generation property management is embracing online payment transfers and reporting for those reasons. This isn’t just green business, it’s good business.

In rental buildings, tenants want to live in a healthier, greener environment. Although this remains difficult to quantify, it makes them feel good about their choice of buildings. There is mounting evidence that tenants are willing to pay a green premium over market rents.

The best way to justify, implement, and embrace change is to regard it as improvement. When property owners consider the multiple advantages of green processes, they need to include the good they do for the environment and their wallets. Better, greener processes should benefit current owners here. Not only will owners lower their current operating costs, but also improve their exit prices down the road. One clear aspect of real estate that future purchasers will investigate is how much a building costs to run. A less clear aspect of real estate value that purchasers look at is how green a building is and what steps management has taken to reduce the carbon footprint. Although difficult to measure, the panache associated with being green translates indirectly to the bottom line. People pay up for and buy more quickly into green property.

This seems a fitting topic as we wind down Earth Month- going green for all the right reasons. The owners who emerge first and best from this market will be the ones who have listened to the market, offer what people want and manage their properties best. As commercial and residential vacancies climb and late payments age, the importance of controlling what you can for your property remains paramount. When your actions can help the planet and line your wallet, so much the better.

Looking for Guidance in This Real Estate Market

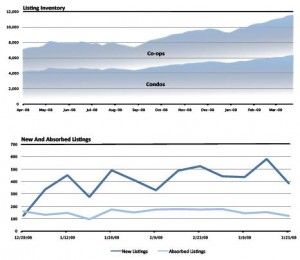

As the value of New York Real Estate evaporates, it has been difficult to accurately measure and report the speed of the decline and where real estate values have held up best. Several sources publish guides from different perspectives using different data.

One of the best, Streeteasy.com’s quarterly guide, came out last week. Aside from painting a bleak picture of the market (sales volume continues to fall) and highlighting neighborhoods where people most overpaid in recent years (Soho), the guide offers a similar purview to other reports such as Corcoran or Elliman with more emphasis on the various stages of residential real estate transactions. Reflecting its web roots, the report uses data cutting across brokerages and delivers detailed stats and graphs.

Market wide stats such as inventory,

Guide for Renters

Tips for Renters

Midtown West: the destination for non-doorman units. Midtown West has long been a neighborhood known for a central location and good value, but that value has gotten even better. With non-doorman units falling over 3% this month, apartments in this area have become an even better bargain. Non-doorman studios are now the lowest priced units, with the exception of Harlem, at $1,670.

Clear choice: LES. If you’re looking for a one-bedroom apartment with service, forget the rest of Manhattan, renters should be combing the LES for deals. One-bedroom units are currently averaging $2,547 – over $450 cheaper than any other central Manhattan location.

Safety, security and service. Battery Park City prices have continued to fall from their heights of last spring and summer. Units in this area are down an average of 14% from their peaks, making them an excellent value for those looking for service and a quieter location.

What does it all mean? There aren’t many surprises here. Values are falling and will continue to fall. Corcoran’s report had a nice conclusion about this, drawing on Robert Shiller, co-creator of the Case-Shiller Home Price Index. “As early as 2005 Shiller predicted severe declines in home prices across the United States. Busts, Shiller argues, follow booms. But just as surely, he says, recoveries follow busts.” In the meantime, property owners need to look for economical ways to differentiate their buildings. There are answers and these answers are not in these published guides.

Condo Dues Defaults Will Punish Unfairly and Scar the Innocents

Financially sound condominium owners will be among the next groups victimized by the credit crisis. While shaky owners default and buildings’ fees rise, that financial burden will fall squarely on the shoulders of better-positioned owners. The problems that led to this situation are sending disastrous ripples to areas that few had predicted. Laws that protect Co-op owners require any repossessing bank to pay maintenance. In a co-op, equity reverts to the building. A condo lacks this protection. With a condominium, the bank has or –in these times- lacks the equity.

Liens, Times and Years. Oh My!

A building can place liens, or threaten to, before the customary three months. Processing a lien can take many years. We got into this financial mess by assuming that existing circumstances will be similar to historical trends. It’s wake up time for the people with the ability to act.

Proactive measures for Condo boards. How early is too early?

Property managers can look for early signs of delinquency. Impose STIFF, eye-popping fines on late dues payers. The owners willing to accept eye-popping penalties are the ones with no choice. This serves as an early warning sign. Proactively filing liens on these condominium owners may get them to repay quickly. It could also be the call to face the music and downsize or seek financial help.

Another less discussed and highly likely scenario is that the courts will become backed up with foreclosure actions. The proactive boards that act swiftly in 2009 are the ones more likely to benefit.

Likely suspects

Owners who financed with no money down and or those who used the 421 tax abatement will face huge increased charges. If 40% of your building’s units have changed ownership in the past 3 years, your neighbors may have taken advantage of easy money and over leveraged themselves.

Blame the Victim?

Looking to victims for help will not provide the best solutions. Although rising delinquencies can lead to finger pointing in the micro-culture of a building (making for tense elevator rides, long board meetings and possibly officer turnover), the people most likely to solve the problem are not the ones who caused it. That unfortunate financial burden will rest with the remaining owners. The time for buildings to offer less and charge more is rapidly approaching.

A difficult pill to swallow

A difficult pill to swallow

To help, buildings can repurpose assets for income generation – storage areas for commercial or medical rentals, rooftops for solar panels or cell towers. Lighting can be switched to high efficiency fluorescent, saving thousands of dollars per year. All systems- ex. furnace gas or oil- can be evaluated for efficiency. These are potential band-aids. In the meantime, many will be injured.

Boards can implement or increase flip charges (transfer fees), and sublet charges and while decreasing required sublet lengths of stay. They can actually welcome sublets in order to increase revenue and to help the struggling owner. Health club hours can be shortened, and other amenities trimmed. These measures have traditionally been associated with Co-ops. We expect to see more condo boards instituting co-ops style policies where possible.

There is no easy fix and the problem will get worse before it gets better. The best way out of this problem is to adopt proactive measures and remain ahead of the curve.

The board of managers…shall have a lien on each unit for the unpaid common charges thereof, with interest thereon, prior to all other liens except only

(i) liens for taxes on the unit in favor of any assessing unit, school district, special district, county or other taxing unit,

(ii) all sums unpaid on a first mortgage of record,